Long-term disability settlement amounts Ontario claimants receive are based on the present value of the monthly benefits you would have collected to age 65, reduced by risk factors and offsets. Insurers often open at 50% to 70% of full value, and that first offer is almost always negotiable. There is no fixed figure, since every policy, age, and medical situation differs.

At Maana Law in Mississauga, our Long-term disability lawyers help disabled clients understand what their claim is truly worth before they sign anything, because a release is final.

What are typical long-term disability settlement amounts in Ontario?

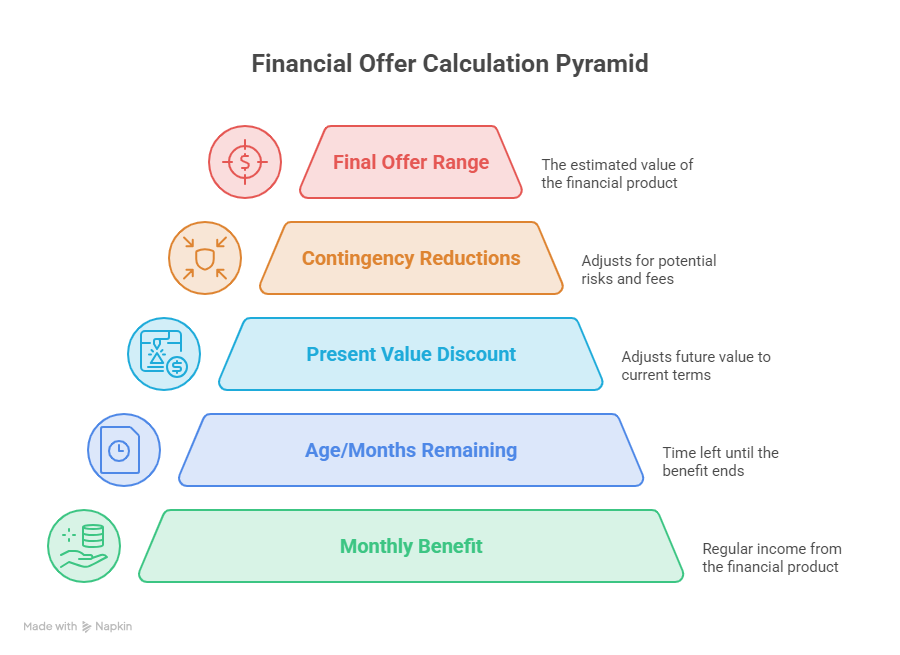

There is no single average, because policies vary too widely. The reliable way to estimate your value is your monthly benefit multiplied by the months remaining until age 65, then adjusted to today’s dollars. A 40-year-old receiving $3,000 per month until 65 is owed far more over time than a 60-year-old with the same benefit. So a true average long-term disability settlement Ontario figure does not exist, but the formula stays constant: the longer your expected disability and the younger you are, the higher the value. For example, suppose a claimant is owed $2,500 per month for ten more years. The total face value is $300,000, but the present value an insurer uses might land closer to $230,000, since a lump sum paid today can be invested and grow. That present value, not the raw total, is the real starting point for talks. For the legal time limits on this kind of claim. For the legal time limits on this kind of claim, see how long after an accident you can sue in Ontario.

How is a lump sum settlement calculated?

A LTD lump sum settlement Ontario offer is built from a few moving parts. Understanding them lets you see where an insurer may be shaving value. The core inputs are your monthly benefit, your age, the policy’s end date (usually 65), and a discount rate that converts future payments into present value. From there, the insurer applies contingencies, the odds that you might recover, return to work, or no longer meet the policy definition of disability.

| Factor | Pushes value up | Pushes value down |

| Age | Younger claimant | Older, near 65 |

| Medical prognosis | Permanent, well-documented | Uncertain or improving |

| Policy definition | Any occupation standard met | Only own occupation period left |

| Offsets | Few collateral benefits | CPP, WSIB, other income |

| Evidence | Strong treating physician reports | Gaps or surveillance issues |

This is why two people with the same monthly benefit can receive very different offers. The Canada Pension Plan disability program can also reduce your monthly figure through offset provisions, which lowers the lump sum too.

What factors affect how much you can get?

The amount depends mostly on how strong your case looks on paper. The single biggest factor is medical evidence. Consistent treating physician reports, a clear prognosis, and continuous medical records signal that your disability is real and lasting. Weak or scattered documentation gives the insurer room to argue you may recover, which lowers the offer. Conditions like understanding understanding chronic pain or catastrophic injuries often carry the strongest medical support because the impairment is well-documented and unlikely to resolve. Other major factors include: Policy definition of disability. Most policies start with an own occupation test, then shift to a stricter any occupation test after about two years. Meeting the tougher standard strengthens your position. Offsets and collateral benefits. Income from CPP disability, Workers’ Compensation, or other sources can be deducted under offset and all-source-maximum provisions. Whether benefits are taxable. This changes the net value in your pocket. Claim handling. Egregious conduct by the insurer can increase value. Strength of your records. Some disabilities are harder to prove than others, which makes thorough documentation even more critical. An independent medical examination ordered by the insurer can cut either way, so it pays to know your rights before attending one.

How do you negotiate a better LTD settlement?

Knowing how to negotiate LTD settlement Ontario offers starts with refusing to treat the first number as final. Insurers expect a counter. The goal is to close the gap between their opening offer and the full present value of your benefits. Strong negotiation rests on preparation. Calculate the present value of your remaining benefits, gather complete medical documentation, and identify any contingencies the insurer is overweighting. When you can show that your prognosis is stable and your evidence is solid, the discount the insurer applies for risk should shrink. For example, a client once received an offer near half of full value. After we organized updated specialist reports and challenged the insurer’s assumptions about recovery, the revised offer rose substantially. The medical record did the heavy lifting; the negotiation simply made the insurer account for it. If you want a clear read on what your offer should look like before you respond, a free consultation with Maana Law can help you see the full picture first.

Are long-term disability settlements taxable in Ontario?

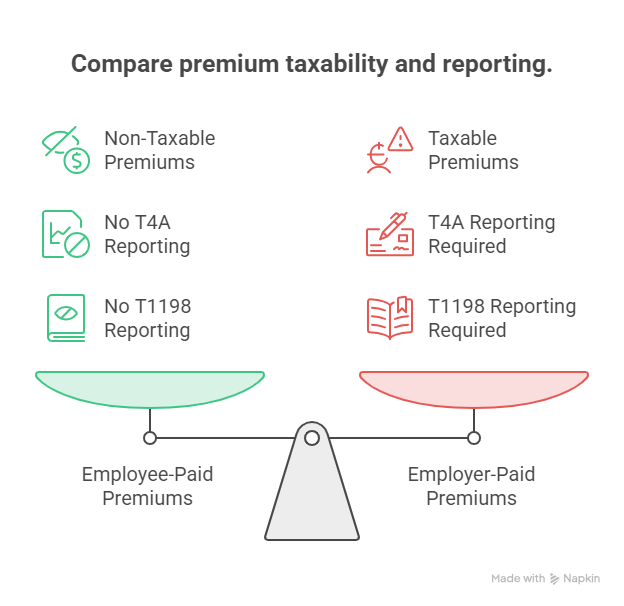

Whether your settlement is taxed depends on one thing: who paid the premiums. If you paid your premiums yourself with after-tax dollars, your benefits and any lump sum are non-taxable. If your employer paid the premiums, the benefits are taxable, and so is the portion of a lump sum that covers past-due benefits. There is a useful wrinkle. On a taxable policy, lumping out future benefits can carry a tax advantage, because the insurer issues a T4A only for past benefits, and future amounts paid as a single sum are generally not taxed the same way. Past-due taxable benefits can also be spread over the years they should have been received using a T1198 form, which can lower the tax hit in the year you receive the money. Always confirm the structure with a lawyer and an accountant before signing.

What happens if your claim was denied?

A long-term disability claim denied Ontario decision is not the end of the road. Denials are common, and many are overturned once a claimant pushes back with proper evidence and legal pressure. You generally have two years from the date of denial to start a court claim in Ontario. That sounds like plenty of time, but you should act early, since civil litigation itself can take many months. Waiting risks both your deadline and your leverage. When you sue, you ask the court to declare that you are disabled under your policy and to order payment of past-due benefits plus interest. Most of these cases settle before trial, often through a lump sum or a reinstatement of monthly benefits with arrears paid. The path you choose, lump sum or reinstatement, should match your health outlook and financial needs.

CPP disability vs LTD settlement: how do they interact?

Understanding CPP disability vs LTD settlement Ontario rules prevents an unwelcome surprise at settlement time. CPP disability and private LTD are separate programs, but most LTD policies allow the insurer to offset CPP payments. If you are owed $2,000 a month in LTD benefits and receive $1,500 from CPP disability, the insurer may only owe the $500 difference. That offset reduces both your monthly entitlement and the value of any lump sum. There is also ODSP to consider. A large settlement can push your assets past ODSP limits, which may affect that support. Planning the structure of your settlement around these programs protects more of your money. An experienced long-term disability lawyer in Mississauga can help structure the payout so it does the least damage to your other benefits.

Why Maana Law is the right choice for your disability claim

Choosing the right advocate changes the math on your claim. Insurers negotiate these settlements every day; most claimants face the process only once. Working with an experienced long-term disability lawyer levels that field. Personal injury and disability focus. We spend our days advocating for injured and disabled clients across all of our practice areas, so we know how insurers value and discount claims. No Win, No Fee model. Our contingency arrangement means you pay legal fees only if we recover for you, removing the cost barrier to strong representation. Accessible, client-first service. Free consultations, virtual meetings, and home or hospital visits make it easy to get help when your health limits your mobility. Clear communication. Led by Aman Kalra, our team explains every offer in plain language so you understand what you are accepting and why. Our clients consistently describe honest guidance and results-driven service. That is the standard we hold on every file.

Frequently asked questions

How long does an LTD settlement take in Ontario?

It varies widely. Some claims settle within a few months once evidence is organized, while disputed claims that head toward litigation can take a year or more. The timeline often depends on how quickly you gather records and whether the insurer disputes your medical evidence. Acting early keeps the timeline shorter.

Should I take a lump sum or keep monthly benefits?

It depends on your health and finances. A lump sum gives flexibility and closes the file, but you may receive less overall and give up future entitlement. Monthly benefits offer steady income but can be cut off again. Understanding the full settlement amounts in civil litigation context can help you weigh what is fair.

Can I negotiate the insurer’s first offer?

Yes. First offers are usually below full value and are expected to be countered. Strong medical evidence and an accurate present-value calculation are your best negotiating tools.

Will a settlement affect my ODSP?

It can. A large lump sum may push your assets over program limits, so the settlement structure should be planned with that in mind.

Do I need a lawyer to settle an LTD claim?

You are not required to have one, but a lawyer helps ensure the offer reflects past benefits, interest, tax treatment, and the true present value of your future benefits. If your disability stems from a catastrophic injury compensation, the stakes are even higher and professional guidance becomes essential.

Conclusion

Settling a long-term disability claim is a major financial decision, and the first offer rarely reflects what your claim is truly worth. Before you sign any release, get an independent read on its value. Contact Maana Law in Mississauga at 90 Matheson Blvd W, Suite 101 for a free consultation. Call us, book a virtual meeting, or request a home or hospital visit, and we will help you protect the full value of your claim before you decide.