Most people who call a personal injury lawyer after a minor accident say the same thing: “I thought I didn’t need one.” By the time they call, they’ve accepted a settlement capped by the Minor Injury Guideline, given a recorded statement to their insurer without medical advice, and signed away rights to compensation for injuries that hadn’t fully developed yet.

Hiring a personal injury lawyer for a minor car accident in Ontario is worth it more often than people expect. Ontario’s insurance system is designed to close your claim efficiently not to ensure you receive everything you’re entitled to.

At Maana Law, we’ve spent over a decade helping Mississauga accident victims recover far more than an insurer’s opening offer by [identifying exactly where minor accident claims break down before they reach a fair resolution]. Here is what this guide covers:

- What the Minor Injury Guideline (MIG) is and how it caps your benefits at $3,500

- When hiring a lawyer makes financial sense and when it genuinely doesn’t

- How much minor injury settlements typically pay in Ontario

- What to do immediately after a collision to protect your claim

- When your insurer’s classification of your injuries can be challenged

Your insurer applied the $3,500 MIG cap — but your injuries may qualify for up to $65,000 in benefits.

Challenging a MIG classification requires the right medical evidence. Maana Law knows exactly what it takes.

What Counts as a Minor Car Accident in Ontario?

A minor car accident in Ontario is generally a low-speed collision where property damage is limited and no serious injuries are immediately visible. Under Ontario’s collision reporting rules, accidents with vehicle damage below $2,000 per vehicle typically do not require a visit to a Collision Reporting Centre (CRC), though municipal thresholds vary.

Common scenarios that fall into this category:

- Rear-end collisions at low speeds or at traffic lights

- Parking lot fender benders

- Minor sideswipes on residential streets

- Low-speed impacts in driveways or private laneways

That definition applies to the collision itself not to your injuries. Whiplash, cervical strain, and soft tissue injuries can result from impacts as slow as 10 km/h. Symptoms frequently do not appear until 24 to 72 hours after the crash. This delay is one of the most significant factors in minor accident claims, because decisions made at the scene or in the first 24 hours can affect your ability to recover compensation weeks later.

Under Ontario’s Direct Compensation Property Damage (DCPD) system, your own insurer processes vehicle repair costs and vehicle replacement costs regardless of who caused the crash. For property damage alone, most minor collision insurance claims Ontario resolve without serious dispute. Where complexity arises is in how your insurer classifies your injuries and what that classification means for your benefits.

What is the minor accident rule in Ontario?

The term generally refers to the collision reporting threshold: if damage falls below the local limit and no injuries occurred, you are not required to report to a Collision Reporting Centre. You remain obligated to notify your insurer, regardless. This reporting rule governs the collision itself and is entirely separate from how your injury claim is processed.

How Does Ontario’s No-Fault Insurance System Work After a Minor Accident?

Ontario’s no-fault insurance system means your own insurer handles your accident benefits after a collision, regardless of fault. You do not need to wait for fault to be determined before accessing medical treatment or income support through your own policy.

Two systems run in parallel after any collision:

Statutory Accident Benefits (SABS): These are the medical, rehabilitation, and income replacement benefits available through your own insurer. To access them, you must file an OCF-1 (Application for Accident Benefits) within 30 days of the accident. Missing this deadline can delay or limit your access to benefits. SABS covers physiotherapy, chiropractic care, lost wages, and rehabilitation costs but the amount you can access depends directly on how your insurer classifies your injuries.

The Tort System: If another driver was at fault, you may have grounds to sue them for additional compensation including pain and suffering damages. Ontario’s tort threshold requires you to prove a “permanent, serious impairment” of a physical, mental, or psychological function. For most minor soft tissue injuries that fully resolve, this threshold is very difficult to meet.

Understanding this two-track system matters because minor car accident settlement Ontario values are often lower than people expect. Your accident benefits address your immediate medical costs. The tort route addresses longer-term losses but only when the injury genuinely crosses the impairment threshold. Knowing which track applies to your situation, and how to position your claim correctly from the start, is one of the clearest reasons legal advice adds value early.

A “minor” accident can produce a $25,000+ claim. The collision size isn’t what determines your payout — documentation does.

Whiplash, soft tissue injuries, and PTSD after a crash all have real settlement value. Let us assess yours for free.

What Is the Minor Injury Guideline (MIG) and Why Does It Matter for Your Claim?

The Minor Injury Guideline (MIG) is a binding Ontario insurance regulation that caps the medical and rehabilitation benefits available to people classified as having “minor injuries” after a car accident. If your insurer places you within the MIG, your total SABS treatment benefits are capped at $3,500 for all treatment combined.

Injuries covered under the MIG include:

- Sprains and strains (muscle, ligament, or tendon)

- Whiplash-associated disorders at grades 1 and 2

- Soft tissue injuries without neurological signs

- Contusions and minor lacerations

- Post-accident headaches without a neurological diagnosis

That $3,500 ceiling applies across physiotherapy, chiropractic care, massage therapy, and all other rehabilitation. According to data tracked by the Ontario Trial Lawyers Association (OTLA), physiotherapy costs for whiplash injuries alone frequently exceed this cap within 10 to 15 weeks of regular treatment.

The deeper problem: Insurers routinely assign claimants to the MIG as a default. They are not required to investigate whether your injuries actually qualify for reclassification. If you have a documented pre-existing condition that the accident aggravated, symptoms consistent with a mild concussion, psychological effects such as post-accident anxiety or sleep disruption, or a latent or delayed-onset injury that worsens over time, you may be legally entitled to exit the MIG and access the non-minor injury benefit pool of up to $65,000.

Challenging a MIG classification requires an OCF-3 (Disability Certificate) from your treating physician, specialist reports, and in many cases the involvement of a personal injury lawyer who understands what medical documentation creates a successful challenge.

Is it worth hiring a lawyer for a minor car accident Ontario?

If your insurer has placed you in the MIG and your treatment costs are approaching $3,500, the answer is almost always yes. A successful MIG challenge can unlock more than 18 times the benefit value of the cap itself.

What a MIG situation looks like in practice:

A client sustains a soft tissue injury and whiplash in a rear-end collision. The insurer applies the MIG cap. Physiotherapy runs at $250 per session the cap is exhausted in 14 sessions. The client still needs 6 more months of treatment. Without legal challenge, that gap comes out of pocket. With a successful MIG exit, the benefit pool increases to $65,000.

If your insurer has applied the MIG cap and you are unsure whether your injuries qualify for reclassification, Maana Law offers free consultations to assess your file before you accept anything call us at 437-979-4878 or book online.

Is It Worth Hiring a Personal Injury Lawyer for a Minor Car Accident in Ontario?

Is it worth hiring a lawyer for a minor car accident Ontario the honest answer is: it depends on specific conditions, not on the size of the collision. A low-speed impact can produce a high-value claim. A multi-vehicle crash can produce no viable claim at all. The collision itself is not the right measure.

Situations where hiring a lawyer typically generates better outcomes:

- Your insurer has applied the MIG cap and your treatment costs are approaching or exceeding $3,500

- Symptoms are progressing rather than improving whiplash, neck pain, back pain, or recurring headaches beyond two weeks

- There is a disputed liability situation or the other driver is claiming you caused the accident

- You received a recorded statement request from your insurer before you had medical documentation

- You are losing income because of your injuries and need support recovering lost wages

- Your vehicle’s loss of vehicle value (diminished value) is being denied

- The other driver or their insurer has initiated a counter-claim against you

- The accident was a hit and run or involved an uninsured driver

Situations where self-managing a minor collision insurance claim Ontario may be reasonable:

- No injuries occurred and all parties agree on that

- Vehicle damage was processed cleanly through DCPD with no dispute

- Your total treatment costs were well under $1,000 and you have fully recovered

- Liability is undisputed and the settlement offer covers all your documented losses

- Your employer provided sick leave coverage and no income was lost

The contingency fee math: Personal injury lawyers in Ontario work on a contingency fee basis. You pay nothing upfront. The fee typically 20 to 33 percent of your final settlement applies only if you recover compensation. On a $25,000 settlement, a 30 percent fee means your lawyer receives $7,500 and you take home $17,500. On the same claim handled alone and settled for $8,000 under the MIG cap, you receive $8,000 but potentially leave $17,000 on the table. The risk of getting advice is low. The cost of not getting it can be significant.

When Should You Hire a Lawyer After a Minor Accident in Ontario?

When to hire a personal injury lawyer Ontario is a timing question as much as a situational one. Earlier is almost always better not because lawyers delay, but because evidence disappears, recorded statements get locked in, and medical timelines begin to matter for the claim.

Right after the accident:

- You are uncertain about who was at fault

- The other driver provided incomplete or potentially false information

- The accident was a hit and run or involved a vehicle that fled the scene

- Police attended and filed a report

Within the first 48 to 72 hours:

- You have developed any pain neck, back, or head even mild

- Your insurer has contacted you requesting a recorded statement about the accident

- You have received a settlement offer before any diagnosis has been made

Within 30 days:

- Your OCF-1 (accident benefit application) must be filed do not miss this deadline

- Your accident benefits have been delayed or denied

- Your insurer is scheduling an Independent Medical Examination (IME), which is an assessment arranged by your insurer not your treating physician to evaluate your injuries and your need for treatment

Within 30 to 90 days:

- Your treatment costs are nearing the MIG cap and your recovery is not complete

- You are being told your psychological symptoms anxiety, sleep issues, fear of driving after the accident are not covered

Ontario’s limitation period for personal injury tort claims is two years from the accident date under the Limitations Act, 2002. This is an absolute deadline. However, [most experienced Ontario personal injury lawyers will tell you that waiting beyond 6 months to seek advice creates real evidentiary problems] that no legal skill can fully overcome lost witnesses, gap-filled medical records, and surveillance that insurers may have already gathered.

When You Can Handle a Minor Car Accident Claim Without a Lawyer

A personal injury claim without lawyer Ontario is appropriate under a specific and narrow set of conditions and those conditions largely come down to the complete absence of any physical injury.

If the accident was a genuine fender bender, there were no injuries of any kind, both drivers exchanged complete information at the scene, and your insurer processed the vehicle damage claim without any issue, a lawyer adds little to the process.

If you experienced mild muscle soreness that resolved within five to seven days and your total treatment costs were well under $1,000, handling the claim directly is reasonable provided you do the following before closing the file:

- Get a medical assessment within 24 hours, even for mild symptoms this creates a contemporaneous record

- Do not sign any release or accept any final payment until you are certain your recovery is complete

- Keep every receipt and record of accident-related costs, including mileage to medical appointments

- Do not give your insurer a recorded statement about how the accident happened without at least a free legal consultation

The risk in handling a small car accident claim Ontario alone is not the process it’s the timeline. Soft tissue injuries and mild concussions often worsen after the initial assessment. If you accept a settlement before the full injury picture is clear and then develop chronic pain or neurological symptoms, that file is closed. You cannot reopen it.

How Much Is a Minor Injury Settlement Worth in Ontario?

Minor accident compensation Ontario values typically range from the MIG cap of $3,500 for fully capped soft tissue claims up to $75,000 or more for minor fractures and injuries with documented long-term effects.

| Injury Type | Typical SABS + Tort Settlement Range |

| Soft tissue injury, MIG cap applied, no challenge | $3,500 (benefit limit only) |

| Whiplash Grade 2, resolved within 3-6 months | $10,000 – $25,000 |

| Cervical strain requiring extended physiotherapy | $15,000 – $35,000 |

| Soft tissue with documented psychological injury | $20,000 – $50,000 |

| Minor fracture (wrist, clavicle, rib) | $25,000 – $75,000 |

Ranges informed by Ontario court data and OTLA member experience. Individual outcomes depend on documented injury severity, recovery duration, and liability position. Verify current precedents with a licensed personal injury lawyer.

What the tort deductible actually means for minor claims: Ontario’s Insurance Act applies a statutory deductible currently approximately $41,503.35 (adjusted annually by CPI) to pain and suffering awards in non-catastrophic tort claims. If a jury awards $55,000 for pain and suffering, the deductible reduces your net recovery to roughly $13,500. If the award is below $41,503, your net pain and suffering amount in tort is zero.

This is not a penalty it is a structural feature of Ontario’s no-fault auto insurance system. It is also the reason why maximizing your SABS recovery (including challenging the MIG where possible) often produces better practical results than pursuing tort alone, particularly for minor injuries.

How much can someone sue for a car accident in Ontario?

There is no legislated upper limit for serious injuries. For minor injuries without permanent impairment, practical tort recovery before the deductible is typically in the $50,000 to $100,000 range. After the deductible, net recovery for pain and suffering is often $8,500 to $58,500 depending on the award. Future medical costs and lost wages are not subject to the deductible and can significantly increase total recovery.

What Do You Do After a Minor Car Accident in Ontario?

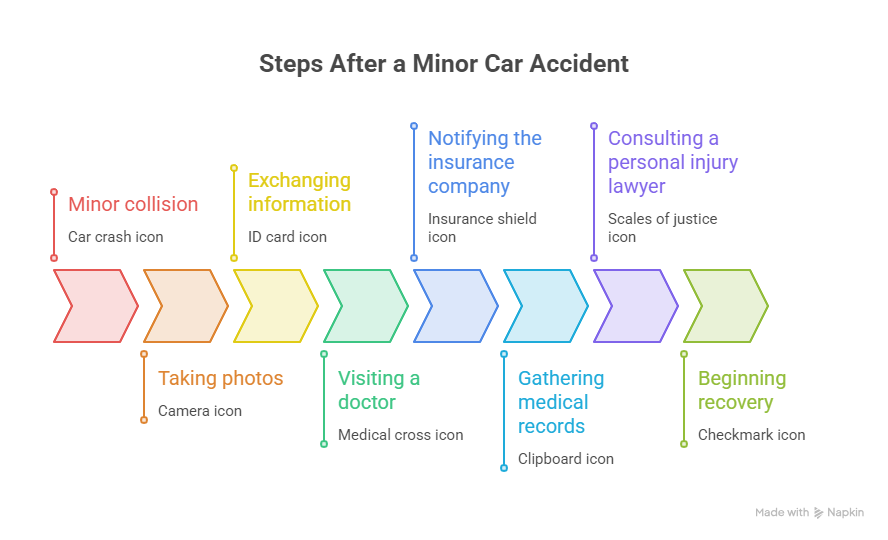

After a minor car accident in Ontario, the first 24 hours determine more about your claim’s outcome than most people realize. These steps protect both your health and your legal position.

At the scene before you leave:

Photograph everything before vehicles are moved: all vehicle damage from multiple angles, the road surface, skid marks, traffic signals, and any visible injuries on yourself or others. Get the other driver’s full name, driver’s licence number, licence plate, and complete insurance information including the insurer’s name and policy number, not just a business card. Collect contact information from any witnesses present.

Within 24 hours:

Visit your doctor or a walk-in clinic. Even if you feel only mild discomfort, a same-day medical record is one of the most protective things you can create for your claim. Delayed injury onset is not unusual after low-speed collisions whiplash symptoms, back pain, and headaches frequently develop the following morning. Document them from the start.

Notify your insurance company. This is a contractual requirement. Failure to report can result in a coverage denial if you later need to make a claim. Your premium impact from reporting depends on your driving record and policy, but not reporting when required is always the worse legal choice.

Within 30 days:

File your OCF-1 (Application for Accident Benefits) with your insurer. This is the formal application for SABS coverage physiotherapy, lost wages, and rehabilitation. Missing the 30-day window does not eliminate your right to benefits, but it creates delays and gives your insurer grounds to dispute coverage.

Should You Tell Your Insurance Company About a Minor Accident?

Yes, always report the accident to your insurer. Ontario auto policies require prompt reporting. Failing to report a collision even one with no injuries can void coverage if a related claim surfaces later. Whether reporting affects your premium depends on your insurer’s at-fault rating system and your claims history.

What Not to Tell Your Insurance Company After a Minor Car Accident?

Do not speculate about fault during your initial report. Avoid saying “I think it might have been partially my fault” before the facts are documented. Do not tell your insurer you are uninjured before you have had a medical evaluation symptoms may develop after your call. Most importantly, do not provide a recorded statement about how the accident occurred before consulting a lawyer, particularly if there is any ambiguity about fault or the extent of your injuries.

Before you close your minor accident file — find out what it’s actually worth. It costs nothing to ask.

Free consultation with Maana Law. In-person, virtual, or home visit. No win, no fee — guaranteed.

Why Maana Law Is the Right Choice for Your Minor Car Accident Claim in Ontario

Not every personal injury firm focuses on the gap between what Ontario’s insurance system pays and what accident victims are actually entitled to receive. That gap is where Maana Law operates and where outcomes are decided.

- MIG challenge experience that directly changes what clients recover. Our team has challenged Minor Injury Guideline classifications on behalf of Mississauga accident victims whose insurers capped their benefits at $3,500. We know which medical evidence triggers reclassification and which specialists produce the documentation that moves an insurer.

- No fee unless your case resolves in your favour. Maana Law operates exclusively on a contingency fee basis. You pay nothing upfront. Our fee comes from your recovery meaning your financial interests and ours are identical from the first consultation.

- Aman Kalra: personal injury law only, not a generalist practice. With over ten years of focused personal injury practice and Law Society of Ontario licensure, Aman Kalra handles accident claims not contract disputes, real estate closings, or criminal matters on the side. Personal injury is the entire practice.

- Accessible support for injured clients. Home visits, hospital consultations, and virtual meetings mean you never need to travel to get qualified legal advice. Free consultations are available from day one.

- Mississauga-based, community-focused practice. Serving clients across Erin Mills, Cooksville, Churchill Meadows, Meadowvale, and City Centre, Maana Law is not a high-volume referral firm. Cases receive individual attention from the lawyer handling the file, not a rotating case manager.

- Verified results for Mississauga accident victims. Maana Law has secured millions in compensation through settlements and verdicts for personal injury clients across soft tissue injury files, MIG challenge cases, disputed liability claims, and catastrophic injury matters.

Getting the right advice early is not a commitment to litigation. It is a commitment to understanding what your case is actually worth before you decide what to do with it.

Frequently Asked Questions

How long do I have to file a personal injury claim after a minor car accident in Ontario?

Ontario’s limitation period for personal injury tort claims is two years from the accident date under the Limitations Act, 2002. However, your OCF-1 (Application for Accident Benefits) must be filed within 30 days of the accident to avoid benefit delays. Certain other insurer deadlines, including the timeframe for disputing a benefit denial, are shorter. Missing any of these timelines can reduce or eliminate compensation you would otherwise be entitled to.

What is the minor accident rule in Ontario?

In Ontario, the minor accident rule refers to the collision reporting threshold. If vehicle damage is below the local reporting limit typically $2,000 and no injuries occurred, you are not required to visit a Collision Reporting Centre. You are still required to notify your insurer promptly under your policy terms. The reporting threshold applies to the collision only; it has no effect on how your injury claim is processed.

Can my injuries qualify for benefits beyond the MIG cap even if the accident seemed minor?

Yes. If you have a pre-existing condition the accident aggravated, symptoms of a mild concussion, a documented psychological injury, or a latent injury that worsens in the days following the crash, you may qualify for reclassification outside the MIG. This typically requires an OCF-3 (Disability Certificate) from your treating physician, specialist reports, and in most cases legal support to pursue the challenge against your insurer.

Does hiring a personal injury lawyer actually increase my net settlement?

In most cases, yes, even after the contingency fee is deducted. Represented claimants generally receive higher gross settlements because lawyers understand the full scope of damages including future medical costs, long-term income loss, and the interaction between SABS recovery and tort claims that insurers do not proactively include in their initial offer. The contingency fee typically ranges from 20 to 33 percent of the final recovery.

What is an Independent Medical Examination (IME) and do I have to attend one?

An Independent Medical Examination is a medical assessment arranged by your insurer not your treating physician to evaluate your injuries and treatment needs. Despite the name, IMEs are paid for by the insurer. You are generally required to attend under your SABS obligations. The report produced often forms the basis for benefit denials or MIG classifications. Speaking with a personal injury lawyer before attending an insurer-arranged IME is strongly recommended.

The Bottom Line on Hiring a Personal Injury Lawyer After a Minor Accident in Ontario

A minor car accident in Ontario can look like a simple property damage exchange at the scene and turn into a months-long battle over whether your whiplash qualifies for more than $3,500 in benefits. The distance between those two realities is determined almost entirely by decisions made in the first 30 days.

Three things matter most. Symptom onset is often delayed after low-speed collisions the absence of pain at the scene does not mean the absence of injury. The Minor Injury Guideline cap can be challenged, but only with the right medical documentation filed at the right time. And because personal injury lawyers in Ontario work on a contingency fee basis, the financial cost of getting professional advice is zero the cost of not getting it, in the right situation, can be measured in tens of thousands of dollars.

Maana Law located at 90 Matheson Blvd W Suite 101, Mississauga, ON offers free consultations for minor accident victims across the Mississauga region. Call 437-979-4878 or contact us online today to get an honest assessment of your claim and find out what your case is worth before you decide what to do next.

References

- Financial Services Regulatory Authority of Ontario (FSRA) — Auto Insurance Consumer Guide: https://www.fsrao.ca/industry/auto-insurance

- FSRA — Superintendent’s Guideline No. 01/14: Minor Injury Guideline: https://www.fsrao.ca/industry/auto-insurance/regulatory-framework/guidance/superintendent-s-guideline-no-01-14-minor-injury-guideline

- Ontario Statutory Accident Benefits Schedule — Ontario Regulation 34/10: https://www.ontario.ca/laws/regulation/100034

- Ontario’s Limitations Act, 2002 — S.O. 2002, c. 24, Sched. B: https://www.ontario.ca/laws/statute/02l24

- Law Society of Ontario — Contingency Fee Agreements and Legal Costs: https://lso.ca/public-resources/finding-a-lawyer-or-paralegal

- Insurance Bureau of Canada — Filing a Car Insurance Claim in Ontario: https://www.ibc.ca/on/auto/claiming

- Ontario Ministry of Transportation — Collision Reporting Requirements: https://www.ontario.ca/page/report-car-accident

- Ontario Trial Lawyers Association (OTLA) — Tort Deductible and Threshold Resources: https://www.otla.com

- Insurance Act, R.S.O. 1990, c. I.8, Section 267.5 — Tort Thresholds and Deductibles: https://www.ontario.ca/laws/statute/90i08