Yes, you can settle a long-term disability claim for a single lump sum instead of monthly payments. The real question behind can I lump sum or settle my long-term disability claim Ontario insurers will agree to is whether you should, and that depends on your medical situation, your policy, and the value of the offer. At Maana Law, our long-term disability lawyers help Ontario claimants understand what an offer is really worth before they sign anything. Here is what this guide covers: How a lump sum settlement is calculated and what reduces it The real difference between lump sum and monthly disability benefits When an offer is fair and when it is too low The deadline you cannot miss when settling a claim Common questions claimants ask before they decide

Can You Settle a Long-Term Disability Claim for a Lump Sum?

Yes. Most LTD policies pay monthly, but insurers often offer a one-time payout to close the file. This is sometimes called a lump sum buyout or policy buyout. A settlement ends the relationship completely. You sign a full and final release, the insurer pays once, and the claim is closed for good. You give up any right to future payments, reinstatement of benefits, or a return to the policy later. Insurers offer buyouts because they reduce litigation risk and remove a long-term liability from their books. You may accept because it gives you a clean break and immediate funds. Both sides weigh the same question from opposite directions: what are years of future monthly disability benefits worth today?

How Does an LTD Lump Sum Payout Work in Ontario?

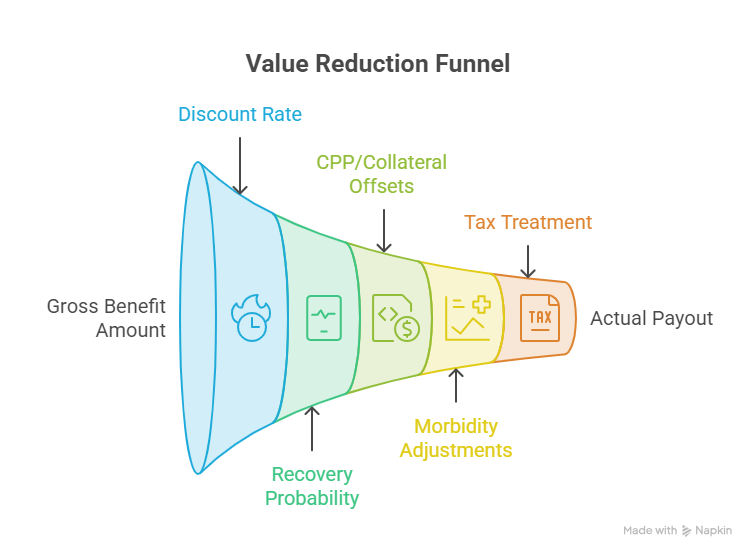

A long-term disability lump sum payout Ontario insurers offer is not simply your monthly benefit multiplied by the months remaining. It is a present value calculation. For a detailed look at how those numbers are built, see our guide on long-term disability settlement amounts in Ontario. Present value reflects the time value of money. A dollar paid today is worth more than a dollar paid in five years, so the insurer applies a discount rate to shrink future payments to today’s value. The higher the discount rate, the smaller the lump sum. On top of that, insurers apply actuarial contingencies. These are reductions for events that might end your benefits early: Recovery probability discount: the chance you improve and return to work Morbidity discount: health and life expectancy factors Cost-of-living adjustment or inflation adjustment, if your policy includes one So a claim with ten years of benefits left will not pay ten years of cash. The insurer estimates your duration of disability, discounts it for risk, then discounts it again for time. This is why two people with identical monthly benefits can receive very different offers.

| Factor | Effect on Payout |

| Strong, permanent medical evidence | Increases value |

| High recovery probability | Decreases value |

| Long benefit period remaining | Increases value |

| High discount rate applied | Decreases value |

| CPP and other offsets | Decreases value |

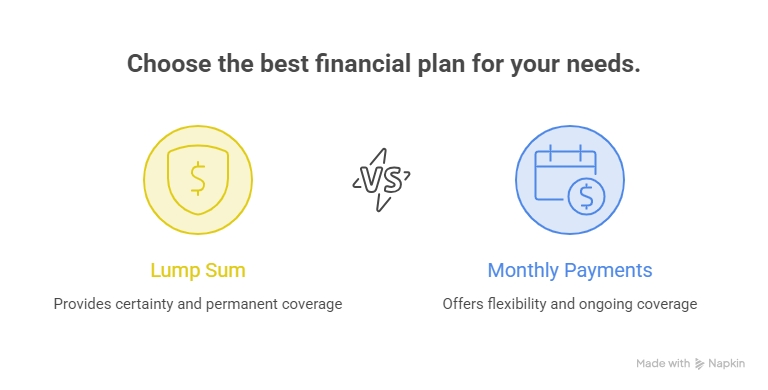

Lump Sum vs Monthly LTD Payments: Which Is Better?

The honest answer to lump sum vs monthly LTD payments Ontario claimants ask about is: it depends on your stability and your needs. A lump sum makes sense when you want certainty, plan to invest the funds, distrust the insurer’s reliability, or have a permanent condition unlikely to change. Monthly payments make sense when your benefits are secure, your condition may improve, or you worry about managing a large sum. Consider a claimant with a permanent disability such as a catastrophic injury and a policy paying to age 65. A lump sum removes the risk that the insurer cuts them off after the next independent medical assessment. Now consider someone recently approved with a recovering condition. Monthly payments may simply continue, and a buyout could undervalue years of future benefits. There is no universal right answer. The right choice is the one that fits your medical reality and your financial plan. Before you respond to any buyout offer, a quick review with the team at Maana Law can confirm whether the number reflects the true value of your claim.

When Should You Accept an LTD Settlement Offer?

Knowing when to accept LTD settlement Ontario insurers propose comes down to one test: does the offer fairly reflect what you would likely win, minus the cost and risk of fighting for it? A long-term disability settlement offer Ontario insurers make is rarely their best number first. Early offers are often low because the insurer is testing whether you will take less to avoid stress. Strong medical evidence strength, clear functional limitations, and a solid prognosis assessment all push the value up. Conditions that are harder to prove injuries require even more thorough records to counter insurer skepticism. Accept when these are true: Your condition is stable or permanent and well documented The offer covers your future loss after fair discounting You include any owed arrears of benefits and prejudgment interest The release language is clear and you understand what you give up Be cautious when the insurer rushes you, when surveillance evidence is being used to dispute your claim, or when the offer ignores extras like waiver of premiums, extended health coverage, or pension contributions. These collateral pieces have real value.

What Affects the Value of Settling a Long-Term Disability Claim?

Several factors decide what a settling long-term disability claim Ontario payout looks like in practice. Your policy definition matters most. Early in a claim, insurers often use an own occupation duties standard, meaning you cannot do your specific job. Later it shifts to an any occupation disability standard, which is harder to meet. Your total disability definition controls how long benefits could last and therefore the lump sum size. Offsets reduce the figure. A CPP disability offset and other collateral benefits are subtracted from your monthly amount before the math even starts. Tax treatment also matters. Whether your benefits are taxable benefits or non-taxable benefits depends on who paid the premiums. Employer-paid premiums usually make benefits taxable, while employee-paid premiums usually make them tax free, which changes net value and tax structuring. Finally, the strength of your file drives leverage. Detailed vocational evidence, consistent treatment records, and a low return to work probability all support a higher number. Claimants living with chronic pain or ongoing functional limitations often have stronger files when continuous treatment records back the claim. In disputed claims, aggravated damages, general damages, or mental distress damages may add value where the insurer acted in bad faith, and pursuing those remedies typically means entering civil litigation.

Is There a Deadline to Settle a Long-Term Disability Claim?

Yes, and missing it can end your claim entirely. Ontario applies a two-year limitation period to sue an insurer, usually running from the date your benefits were denied. This deadline is set by the Ontario Limitations Act, and courts enforce it strictly. If you do not settle and the deadline passes without filing a statement of claim in the Superior Court of Justice, you can lose the right to recover anything, no matter how strong your case. Some policies also require you to use an internal appeal process first, but appeals do not always pause the legal clock. This is the single most common way claimants lose leverage. Once the limitation period is gone, the insurer has little reason to negotiate. Track your denial date carefully and get advice well before two years pass.

Why Maana Law Is the Right Choice for Your LTD Settlement

Settling a disability claim is one decision you only get to make once. The team at Maana Law focuses on personal injury and disability matters for clients across Mississauga and the Greater Toronto Area, with over a decade of combined experience securing fair results. Honest valuation of your offer We review the present value math and offsets so you know if the number is fair before you sign. No Win, No Fee policy You pay nothing upfront. Our fee comes only if we recover for you. Free, accessible consultations We offer virtual meetings and home or hospital visits when travel is difficult. Clear communication at every step You get straight answers, not legal jargon, and updates you can actually follow. Local, client-first advocacy We serve Mississauga communities including Erin Mills, Cooksville, Lorne Park, Churchill Meadows, and City Centre. Our goal is simple: make sure you understand your options and never settle for less than your claim is worth.

Frequently Asked Questions

Can the insurer force me to take a lump sum?

No. A buyout is an offer, not a requirement. You can accept it, negotiate it, or keep your monthly benefits. The insurer cannot end your benefits just because you decline a settlement.

Is an LTD lump sum settlement taxable in Ontario?

It depends on the policy. If you paid the premiums, the payout is usually tax free. If your employer paid them, the benefits and settlement are often taxable. Confirm before you accept.

Can I reopen my claim after I settle?

No. A full and final release ends the claim permanently. There is no reinstatement, even if your condition worsens later. This is why fair valuation upfront is critical.

How long does it take to settle a long-term disability claim?

It varies. Simple buyouts can close in weeks, while disputed claims may take many months. Strong medical evidence and clear documentation usually speed things up. Our guide on whether to settle or go to trial covers the factors that affect timeline.

Do I need a lawyer to accept a settlement offer?

You are not required to have one, but a long-term disability lawyer can spot a low offer, calculate present value correctly, and negotiate hidden value like arrears, interest, and benefit offsets.

Conclusion

A lump sum trades future monthly benefits for certainty today, but only a fair offer protects you. The wrong choice, or a missed two-year deadline, can cost you years of benefits you cannot get back. Before you sign anything, find out what your claim is truly worth. Ready to find out what your offer is really worth? Contact Maana Law in Mississauga, ON at 90 Matheson Blvd W, Suite 101 for a free, no-obligation consultation. We work on a No Win, No Fee basis, so reach out today before any deadline passes. This article is general information, not legal advice. Speak with a licensed lawyer about your specific situation.